If you’re trying to buy your first home in Cumbria, the market has shifted in your favour in several areas.

West coast prices are dropping fastest, making starter homes more accessible.

Lake District prices are easing, offering rare chances in premium villages.

And the industrial corridor remains stable, giving buyers predictable long-term value.

Our postcode-by-postcode map reveals exactly where the pressure is hitting right now, with wide variations across our county.

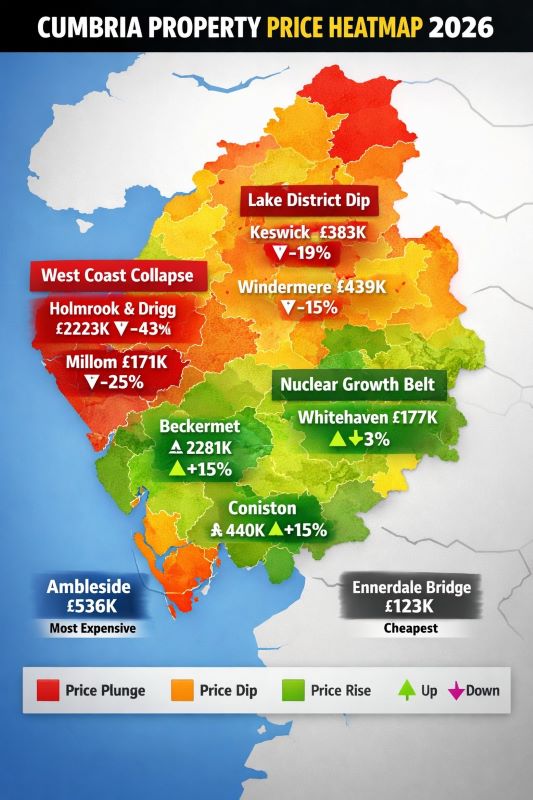

The biggest drop is centred on the CA19 Holmrook and Drigg patch, where prices have plummeted by 43 per cent on the year to April, marking the steepest fall anywhere in Cumbria.

Just down the coast in Millom, has dropped by 25 per cent, pushing it deeper into the red zone. Ravenglass, Moor Row, and Frizington all sit in the same bracket, each posting double-digit falls.

For homeowners and commuters traveling the A595 daily, this entire stretch is now the county’s hardest-hit corridor.

Further east, the Lakes are showing a ‘premium erosion’ pattern.

Keswick, is down 19 per cent, while Windermere has dipped by 15 per cent.

Even Ambleside, usually considered bulletproof by TV’s Homes Under the Hammer, has slipped by nearly 10 per cent – though it still holds the county’s highest average price tag at £536,000.

The only clear growth is running straight through the ‘nuclear belt’, driven by stable industrial employment and new project investment.

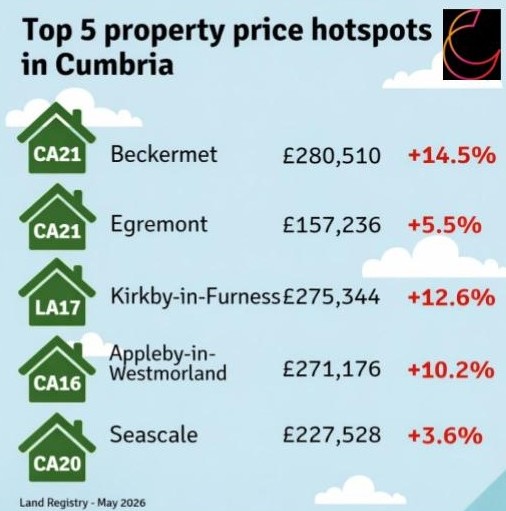

Beckermet is up 14 per cent, Egremont has risen by 5 per cent, and both Seascale and Whitehaven have posted small but steady rises.

This green zone marks the county’s only significant upward trend.

Meanwhile, the South Lakes has produced a few selective winners, with Coniston rising 15 per cent and Kirkby-in-Furness up 12 per cent.

At the absolute extremes of the Cumbrian market, Ambleside remains the most expensive place to buy a house, while Ennerdale Bridge stays the cheapest with an average price of £123,000.

Regional house builder perspective: A ‘measured’ rather than subdued market for Cumbria

While the data shows sharp contrasts between falling premium zones and climbing industrial corridors, the shifts are viewed as a sign of the market returning to a normal rhythm after years of frantic activity.

“From our perspective, the Cumbrian housing market has become much more measured over the last 12 months,” says Nicky Gordon, managing director of Genesis Homes.

“Buyers are taking longer to make decisions than they were a couple of years ago, and affordability continues to be influenced by higher interest rates and the wider cost of living.

“That said, demand for quality new homes remains resilient, particularly where developments are well located and offer strong value for money in the long term due to the sustainability credentials of new build homes.

“We’re also seeing a more discerning customer. Buyers are carrying out greater research, comparing products more carefully and expecting high standards of specification, energy efficiency, and customer service.

“Looking ahead, there is cautious optimism. As borrowing costs continue to ease and consumer confidence gradually returns, we expect activity to strengthen.

“Cumbria has strong long-term fundamentals, including significant inward investment, employment growth linked to major infrastructure and defence projects, and continued demand from people choosing to live and work in the county.

“The key challenge for the industry remains delivering enough new homes at a time when planning, infrastructure, and regulatory requirements continue to become more complex and costly.

“Overall, I would describe the market as stable rather than subdued. The pace has normalised, but the underlying demand for good-quality homes in Cumbria remains strong.”

How the changes group together

West coast – Collapse zone (Red)

- CA19 (Holmrook & Drigg): £223,464.30 (▼ 43.49%)

- LA19 (Millom): £171,200.00 (▼ 25.36%)

- CA18 (Ravenglass): £224,983.30 (▼ 17.79%)

- CA26 (Frizington): £150,022.20 (▼ 15.81%)

- CA24 (Moor Row): £124,426.60 (▼ 15.13%)

Lake District – Premium erosion (Amber)

- CA12 (Keswick): £382,518.10 (▼ 18.94%)

- LA23 (Windermere): £438,602.80 (▼ 14.71%)

- LA20 (Broughton-in-Furness): £321,722.20 (▼ 12.73%)

- LA22 (Ambleside): £536,178.90 (▼ 9.78%)

Industrial/nuclear corridor – Growth zone (Green)

- CA21 (Beckermet): £280,510.00 (▲ 14.53%)

- CA22 (Egremont): £157,235.60 (▲ 5.51%)

- CA20 (Seascale): £227,528.20 (▲ 3.58%)

- CA28 (Whitehaven): £176,920.60 (▲ 3.35%)

South Lakes – Selective winners (Green)

- LA21 (Coniston): £439,821.40 (▲ 15.42%)

- LA17 (Kirkby-in-Furness): £275,343.80 (▲ 12.60%)

Market towns – mixed (Amber)

- CA16 (Appleby-in-Westmorland): £271,175.50 (▲ 10.22%)

- CA5 (Dalston): £318,731.20 (▲ 3.25%)

- CA14 (Workington): £165,157.90 (▼ 9.08%)

County extremes

- Most expensive: LA22 (Ambleside) — £536,178.90

- Cheapest: CA23 (Ennerdale Bridge) — £123,054

{kind=link}